An introduction to blockchain in ecommerce

Blockchain provides the backbone for a new breed of internet. And with exciting use cases across online retail and far beyond, it’s little surprise that ecommerce giants are jumping on the technology, from Walmart to Unilever.

But what exactly is it and what does the ecommerce blockchain opportunity really look like? Let’s take a look.

What is blockchain (in a nutshell)?

A blockchain can be defined as a chain of online transactions usually carried out in cryptocurrencies and saved as a shared ledger across numerous computers on a peer-to-peer network.

Blockchain technology is considered one of the greatest technological advances in recent history and is based on various forms of software engineering, cryptographic science, economic game theory, and disruptive computing.

Where did blockchain come from?

Blockchain technology was invented in 2008 by ‘Satoshi Nakamoto’. The intention was for it to serve as public transaction ledger for Bitcoin, a cryptocurrency.

The invention of blockchain for Bitcoin made it the first digital currency capable of solving the double-spending challenge without the need for a central server.

What is it used for?

Blockchains have the potential to shape the way society works. The have almost limitless applications and use cases across the likes of online retail, supply chain management, money transfers, digital IDs, real estate management, data sharing, food safety, immutable data storage, tax compliance / regulation, and digital voting, and so on.

What kind of technology does it use?

Blockchains consists of a combination of technologies as has been defined previously.

Nonetheless, the very top-level aim of blockchains is to ensure transactional integrity and anonymity. These aims are obtained using the following two pieces of technologies:

Asymmetrical cryptography

This type of encryption is so widespread that most people are utilising it on a daily basis without actually realising. Messaging apps such as Whatsapp use a form of asymmetrical encryption in order to keep the contents of messages hidden from third-party eyes.

The concept of private key cryptography can be best explained using the analogy of two people each carrying different keys and interacting on an online platform.

In this case, the first individual holds a private key while the second holds a public key.

By combining the private and the public keys, the idea of cryptography allows the two people to produce a secure digital identity reference point.

The following is an example of a simple asymmetrical cryptographic dialogue between two people:

This is one of the major components of a blockchain. A combination of the two keys generates a digital signature that is used to control and certify ownership of a ‘block’ within the blockchain.

The digital signature is then combined with a distributed network technology to form a pool of individuals who can interact and act as validators to reach an agreement about various things including online transactions. The process is mathematically certified and is used for network security.

Typically, this digital signature is the only visible piece of information which links back to a user, thus allowing a degree of personal anonymity.

Shared ledger

A shared ledger is a set of data which has been consensually distributed and synchronised amongst those who have access to the blockchain itself.

The advantages of having a shared ledger is that transactions carried out on a blockchain are recorded onto the ledger, which is then distributed geographically to other people around the world who are using the same blockchain network, with users subsequently acting as ‘witnesses’ to each transaction carried out on the blockchain.

By allowing participants to view every change made on the blockchain network instantaneously, while also allowing them to obtain a ‘copy’ of the transactions, the shared ledger prevents entities from maliciously attacking or manipulating data within the blocks of the network.

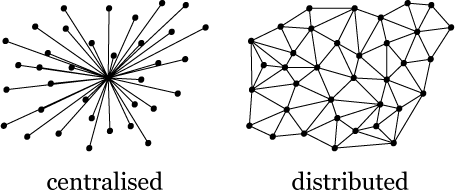

This technology is at the forefront of decentralisation. It allows full transparency of all transactions being carried out on the network and removes the need to have a central authority checking the validity of those transactions.

An example that helps explain this technology is Google Docs. When a user creates a shared document on Google Docs, he or she can give access to outside sources thus resulting in the document acting as a shared ledger.

Subsequently any changes made by those who have access to the document will be instantly shared and distributed. By allowing this to happen, a single user cannot carry out changes discreetly and can easily be held accountable by others for any changes carried out to this shared document.

This technology is at the forefront of decentralisation because it allows full transparency of any transactions being carried out on the network and removes the need to have a central authority checking the validity of those transactions.

Image courtesy of Shyam Shankar, Medium

The generated digital signature can be combined with distributed network technology to create a group of people who can carry out transaction validation and arrive at an agreement about the online transactions. This process has been certified mathematically and is used to secure the network.

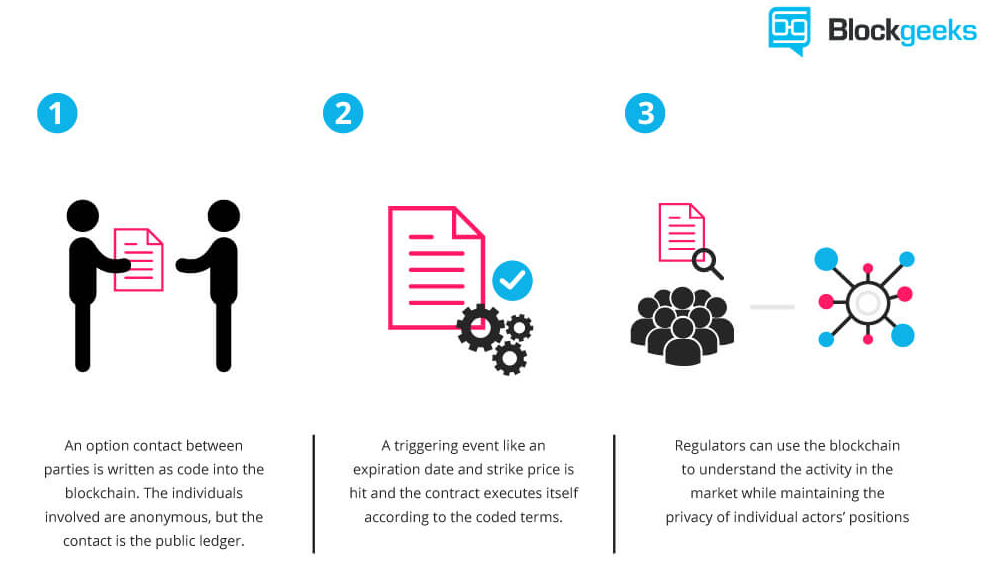

What's more, this combination between distributed networks and cryptographic keys has enabled blockchains to accommodate various types of usage such as: asset ownership, digital voting, identity verification and smart contracts, amongst others.

Smart contracts using blockchain: illustration courtesy of Blockgeeks

What is the lifecycle of a blockchain transaction?

The best way to understand the lifecycle of a transaction in a blockchain is by using a real-world example.

Let’s go back to our favourite non-couple, Troy and Anna. After getting rejected by Anna, Troy has desperately resorted to winning Anna’s love through the use of money. Troy knows that Anna is an avid cryptocurrency trader, so he wants to send her a Bitcoin.

So how exactly will this transfer work?

The first stage: Troy uses fiat money to purchase a Bitcoin from a cryptocurrency exchange such as Coinbase. He then obtains Anna’s public wallet address, which she uses to store her own Bitcoins. Using that wallet’s address he confirms that he wants the transaction to take place.

The second stage: Troy’s pending transaction is then placed in a ‘block’ which consists of thousands of transactions also waiting to be verified, and then broadcasted to millions of nodes which act to ensure the transaction has met all of the rules set by the network.

The third stage: These transactions are then grouped together and placed in a ‘block’. Each block is the given its own unique hash (254-bit number) which is generated using a complex algorithm.

The contents of the block itself includes the current block’s hash, the previous successful block’s hash, and the digital signatures of the pending transactions within that block.

The fourth stage: Each mining node (device used to verify the validity of the network’s transactions) will then compete against each other to crack a highly complex mathematical puzzle as derived from the block’s hash. The puzzle is used in order to verify that the contents of the transaction meets the criteria set by the Bitcoin network, this is referred to as ‘proof-of-work’.

To put into perspective the complexity of these puzzles, blockchain news site BlockExplorer has cited that the probability of cracking one as 1 in 5,800,000,000,000!

Due to the puzzle’s high complexity, thousands of mining nodes are often combined in order to solve a single block’s hash puzzle, often using an absurdly large amount of electrical energy in the process.

Why do people bother ‘mining’? Simple. When a mining node successfully solves the complex puzzle, the winning node then automatically announces the victory to rest the network, which will in turn, force other mining nodes to give up and move on to cracking the next block’s hash puzzle.

The victorious node will then be rewarded with a set amount of Bitcoins for its troubles, currently set at 12.5 Bitcoins (~£35,000).

The final stage: Once a block has been solved, the blockchain nodes will then distribute the successful block throughout the network, thus adding the new transactions to a shared ledger.

The outcome: Troy’s Bitcoin appears in Anna’s wallet. However, Anna is not impressed by Troy’s persistency and files a restraining order against him.

Ecommerce blockchain: the benefits

Interest in blockchain has spread like wildfire in the technology world over the past few years, with large companies such as Microsoft, IBM and Visa investigating how they can adopt the technology within their ecosystem to pave the way for a Web 3.0.

It’s no surprise either, the benefits of utilising blockchain technology could potentially be a game-changer. Here are a few reasons why:

Cheaper transactions

The cost of transactions in a blockchain is lower than that of traditional ecommerce. For instance, public blockchains charge a fee of about $0.01 for every transaction with private blockchains offering even lower charges. This makes blockchain highly preferable for digital transactions.

The low costs incurred in blockchain transactions have subsequently opened the door for rapid micropayments.

By almost eradicating the payment processing fees enforced by card companies and banks, online retailers would then be able to pass on the savings to customers through cheaper product costs.

Faster transactions

Compared to traditional payment systems, blockchains allow faster transactions. For example, a payment processing company called Monetha in the recent past noted that traditional payment systems involves up to 16 different phases.

This involves a fee of between 2% and 6% of the total transaction amount thus resulting in a far more expensive and lengthy processing time when compared to transactions made on a blockchain.

Transactions in blockchains are carried out in a single network without the need for intermediaries. So transaction speeds are only limited by the network’s capacity.

Bitcoin, for example, can handle up to seven transactions per second while other platforms such as Ethereum’s ‘Lightning Network’ can potentially handle up to one million transactions a second.

Data security

By having data distributed amongst a network consisting of more than a million computers, this technology is seen as both reliable and immutable.

Rather than storing data on a server, blockchains are decentralised. Companies have peace of mind, knowing that an outsider would be unable to hack into their data and carry out unauthorised actions.

As the decentralised data is encrypted and cross-checked by numerous nodes on the network, infiltrating the network would be extremely difficult and expensive as each node on the network would fight back against any attack carried out on the blockchain. And so bypassing this defence would only be possible by simultaneously infiltrating a majority of nodes located all over the planet, otherwise known as a ‘51% attack’.

Similarly, decentralisation is key to data reliability. Having data scattered in an identical fashion across millions of nodes, companies are more protected from data loss due to server failures and catastrophes.

Purchase history

Storing historical sales data can often be a challenging task for some companies who make a vast amount of sales on a regular basis.

Using a blockchain to store details of all historical purchases means that proof of ownership is both immutable and impossible to lose.

This logic can also be used to enforce item warranties. Having an impenetrable form of transactional data, companies can also easily figure out how authentic proof of ownership is when it comes to validating warranties.

Supply chain tracking

How often have we heard of retailers using questionable tactics to cut costs at all stages of the supply chain? Companies have countlessly fallen foul of unethical practises such as using cheap labour, poor quality parts, and genetically modified food being passed off as ‘organic’.

The immutable and transparent nature of blockchain technology eradicates this issue by holding each stage of the supply chain accountable for its origin. As the data cannot be altered, retailers, and more importantly customers, will ultimately gain trust by knowing that the source of each product can be transparently tracked throughout its lifecycle in an authentic manner.

New payment methods

Digital currency as a means of payment is something retailers will be giving serious thought in the near future.

Why? Because numerous cryptocurrencies are offering solutions to problems brought about by traditional fiat currencies.

By using cryptocurrency as a payment method, payment gateways become a thing of the past as the risk of fraud is greatly reduced due to the aforementioned immutability of blockchains.

What’s more, peer-to-peer cryptocurrencies are instantaneous since the ‘middle-man’ is cut out from the picture, saving a vast amount of processing time and money.

Retailers using blockchain right now

As the retail landscape changes rapidly, falling behind the herd can often have fatal implications for businesses.

That’s why it’s no surprise that industry giants are leading the way when it comes new technologies such as blockchain.

Below are examples of how this technology is playing a key role in their business models:

Maersk

Being the largest shipping company in the world, a vast number of retailers will, at some point, call upon the services of Maersk.

In partnership with IBM, Maersk is utilising blockchain technology for a system called TradeLens which delivers transparent shipping-lifecycle data in real time to those who play a part in the supply chain.

This technology will also reduce human error and significantly speed-up the shipping process by enabling the automation and digitisation of shipping paperwork, something which Maersk says represents one fifth of the total shipping cost alone.

If this technology becomes widespread the benefits of these lower shipping costs will be felt across the ecommerce world. Savings will be passed onto customers as products become cheaper as a result.

Walmart, Nestlé, and Unilever

These retailing giants have also partnered up with IBM to deploy blockchain technology in order to increase food trust.

When it comes to supply chain management in the food industry, traceability plays a pivotal role in ensuring customers aren’t faced with scandals similar to Tesco’s horse meat fiasco a few years ago.

Ensuring food fraud is kept to a minimum, the use of Walmart’s system ensures that all data related to every piece of food item is tracked using a distributed ledger. This data can then be stored securely and used by anyone in order to understand where the product has originated from and where it has been.

An example of when this would be extremely helpful would be if a specific farmhouse fails a hygiene inspection. The meat from that specific farmhouse can be tracked down easily and disposed by the retailer or even the customer.

Blockchain technology enables a new era of end-to-end transparency in the global food system. It's equivalent to shining a light on food ecosystem participants that will promote responsible actions and behaviours.

What’s the future of blockchains?

As the hype around this grows with each passing day, more and more large institutions are coming to the realisation that this could very well be a market disruptor in numerous use cases such as online retail, supply chain management, voting, and, more obviously, banking and finance.

Like all new and emerging technology, blockchain development is still in its infancy and isn’t perfect.

But developers are making daily improvements to encourage widespread adoption across all aspects of society, with the World Economic Forum predicting that this technology will boost global trade by $1 trillion within the next 10 years.

One thing is for sure though: now that we’ve figured out the benefits of this technology, harnessing its potential will be pivotal in confirming whether this truly is one of the greatest technological advances ever made.